3 Stocks That Could Surge Over 30%

Investors are still uncertain just where the stock market is headed. Essentially, there are two competing opinions right now. One says that we’re just in a bear market rally, and that the worst is yet to come. The other thesis states that the current rally is real, and will mature into a new bull cycle as the economy restarts in the second half.

Writing from JPMorgan, Marko Kolanovic, the investment bank’s quant analyst, holds fast to that optimistic view. Kolanovic believes that epidemiological data suggests we are past the worst of the coronavirus spread, justifying the lifting of social and business restrictions. And that will open up economic activity, which will then find stimulus from low Fed interest rates and increased government ‘pump priming’ spending.

Kolanovic sees the stimulus policies as more important than Q1’s weak earnings, writing, “The combined suppression of the risk free rate and credit spreads by the Fed likely has a bigger positive impact on equity valuation, compared with the negative impact of the temporary earnings loss.”

Kolanovic is not the only JPM analyst who sees potential in the stock markets. The firm’s equity analysts have been working overtime to find the stocks best positioned to lead a potential bull rally. We’ve used the TipRanks database to pull up three of their stock picks, to find out why the JPM experts are tapping them for over 30% growth.

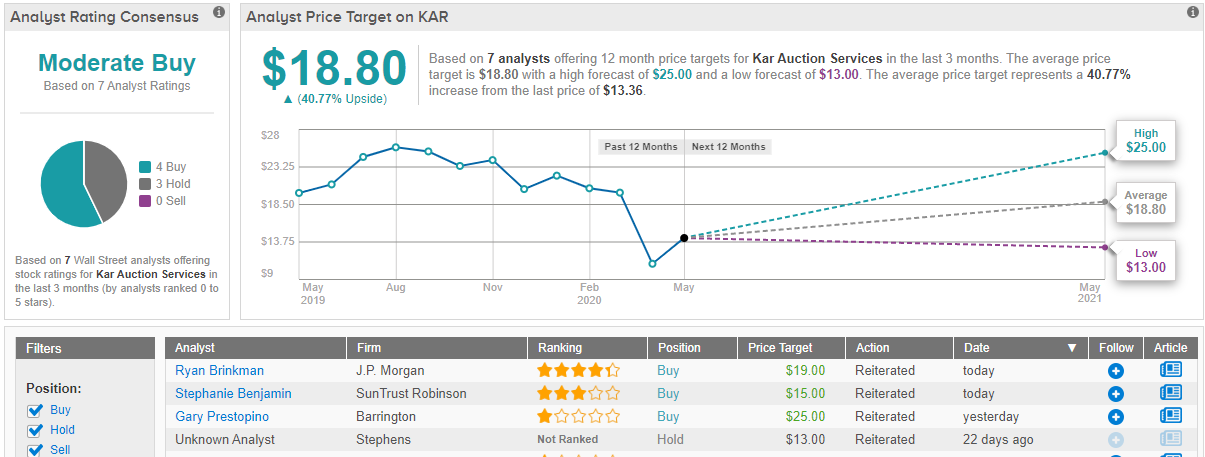

KAR Auction Services (KAR)

The first stock on our list belongs to a company in the second-hand vehicle market. KAR Auction Services operates a marketplace – both online and in the physical world – for used vehicles. The company sells to both individual and business buyers, people looking for a car to drive and garages looking to source parts for the shop floor. KAR sold over 3.7 million vehicles in 2019, bringing in $2.8 billion in auction revenue.

KAR shares have been hit hard by the coronavirus epidemic. The combination of economic shutdowns and social lockdowns have not just put a hold on car sales – they have simply reduced the need for vehicles.

Q1 earnings showed a 6% reduction in revenue, to $645.5 million, and a collapse in net income to $2.8 million from $15.3 million in the year-ago quarter. As noted, these steep reductions are attributable to the effects of the pandemic response. KAR shares are still down 38% year-to-date, badly underperforming the broader markets.

However, JPM’s analyst Ryan Brinkman believes the current downturn is the time to buy in to KAR shares. The low price offers an attractive point of entry, and the stock has a clear path forward when economic activity resumes. Brinkman writes, “We believe that once stay-at-home orders are lifted and the situation moves from being one of a unique public health crisis to that of a more familiar economic downturn, aftermarket end-markets, including auctions, will earn their reputation for resiliency. People will drive again substantially similar to before, and volumes will return to salvage auctions.”

Along with that optimistic assessment, Brinkman upgrades KAR from Neutral to Buy. His $19 price target suggests a strong 46% upside potential in the next 12 months. (To watch Brinkman’s track record, click here)

Overall, KAR shares hold a Moderate Buy rating from the analyst consensus, which breaks down into 4 Buy reviews and 3 Holds. While the analyst corps is somewhat divided, their average price target is in line with Brinkman’s. (See KAR stock analysis at TipRanks)

J2 Global Communications (JCOM)

Next up is an internet communications company. J2 Global owns a diverse portfolio of 40+ online content brands, including IGN, Mashable, PCMag, BabyCenter, Everyday Health among others. In addition, J2 also runs a Cloud Service business, offering eFax and eVoice among other online services. The company boasts nearly $1.5 billion in annual revenue, and saw Q4 earnings rise to $2.19 per share.

The Q4 earnings were the highest in two years, and capped a full year of rising earnings. Q4 is typically J2’s strongest quarter, while Q1 is typically the weakest, so the $1.35 estimate for Q1 earnings is less indicative of poor performance than one may think at first. On an important note, that Q1 estimate represents a modest increase of 1.5% year-over-year.

JCOM shares’ price performance has roughly mirrored the broader market’s during the past three months. JCOM lost 35% in the initial slide, and has risen 21% from its trough.

Initiating coverage of the stock for JPM, Cory Carpenter set a Buy rating, with a $105 price target that indicates room for 32% upside growth. (To watch Carpenter’s track record, click here)

Supporting his stance, Carpenter notes the company’s strong Cloud position, writing, “We believe Cloud Services is well positioned to capitalize on growing security & privacy needs, with bundling & cross-sell potential, and we like that Digital Media monetizes through multiple rents—ads, subs, & affiliate commerce.”

Key drivers for Carpenter’s bull thesis include: “1) Total growth strategy drives sustainable growth, with $1B+ capital to deploy […] 2) Diversified portfolio of leading Cloud Services & Digital Media brands. […] 3) Strong FCF generator with M&A flywheel. JCOM prioritizes FCF, not growth at all costs, which it largely redeploys into M&A. JCOM’s 40% EBITDA margin is driven by Cloud Services’ ~50% margin and Digital Media’s ~35% margin.”

Carpenter is broadly in line with the rest of Wall Street, which has assigned JCOM more “buy” ratings than “holds” over the past three month — and sees the stock growing about 26% over the next 12 months, to a target price of $101.30. (See J2 Global stock analysis on TipRanks)

Montage Resources Corporation (MR)

Last on our list is a small-cap hydrocarbon exploration and production company. Montage is based in the Appalachian region of Pennsylvania, Ohio, and West Virginia, where it operates natural gas and crude oil drilling wells. Montage holds over 195,000 undeveloped core acres, and operates 325 actively producing horizontal wells. The value of the company’s holdings is clear from its stock performance; in the last three months, while the markets have generally slid into a bear cycle, MR shares have gained 55%.

Even with the COVID-19 epidemic and the collapse of oil markets, MR was able to increase its net daily production during Q1, reaching 6610.7 MMcfe. This was above both company guidance and analyst estimates. Quarterly income of $62.7 million also beat the expectations. The company has curtailed some production in low-margin crude oil, to compensate for the soft oil market prices.

Analyst Arun Jayaram, reviewing MR for JPM, upgraded his stance on the shares from Neutral to Buy. His $8 price target implies a 43% upside growth potential for the coming year. (To watch Jayaram’s track record, click here)

Jayaram is clear on his reasons for upgrading this stock. He says of MR, “We expect the market to largely look through negative estimate revision risk to 2020 forecasts to the emerging bullish natural gas narrative in 2021… Meanwhile, the company’s FCF yield of 23% leads the peer group and is well above the peer group average of 10%…”

The Strong Buy analyst consensus on MR shares is based on 5 recent reviews, including 4 Buys and a single Hold. The company’s strong natural gas production is tangible asset, and its enviable free cash flow is attractive for investors. Shares are selling for $5.59, while the average price target of $6.22 suggests a modest upside of 1.6%. (See MR stock analysis at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.