Morgan Stanley Is Getting Bullish About Biotech; Here Are 2 Stocks to Buy

2020 will be remembered as the year of the biotech sector. Amid the ongoing pandemic, biotech stocks have taken center stage, with the names developing COVID-19 solutions being catapulted to remarkable highs. But, after posting such jaw-dropping gains, where do these stocks go from here?

Morgan Stanley’s Chief U.S. Equity Strategist Mike Wilson says the story could get even better. Doubling down on his optimistic stance, he argues stimulus packages that support consumer demand as well as cost-cutting measures could be catalysts that spur strong showings in 2021.

“We think that a return of topline growth and a material reduction in the cost base will lead to operating leverage flow through that such that peak profits will appear again before peak sales… We’ve seen margin upside drive earnings growth coming out of prior recessions and expect the same this time, with potential further upside from massive fiscal stimulus,” Wilson wrote in a recent note.

Taking Wilson’s outlook into consideration, we wanted to learn more about two biotech stocks receiving a standing ovation from Morgan Stanley. However, given the risk involved with these plays, we used TipRanks’ database to get a second opinion. As it turns out, both tickers have earned a “Strong Buy” consensus rating from the rest of the Street.

ACADIA Pharmaceuticals Inc. (ACAD)

Hoping to improve the lives of patients with central nervous system (CNS) disorders, ACADIA Pharmaceuticals is working to bring its cutting-edge therapies to market. Even though shares fell after the company announced it would no longer be pursuing a broad major depressive disorder indication, Morgan Stanley believes the valuation is attractive.

Writing for the firm, analyst Jeffrey Hung tells clients that much of ACAD’s pipeline is related to different indications for pimavanserin, which was approved as Nuplazid in 2016 for Parkinson’s disease psychosis (PDP). He argues the therapy could “expand into a market 10x the size with potential approval for dementia-related psychosis (DRP) by April 3, 2021.”

It should be noted that the Phase 3 HARMONY trial in DRP was stopped early for positive efficacy in September of last year as pimavanserin met the primary endpoint, with the supplemental application submitted in June. “DRP opens up the opportunity to treat an additional 1.2 million patients (vs. roughly 120,000 with PDP) and could drive an additional $3 billion-plus in peak sales. Based on the current share price, we believe the market does not ascribe much value to negative symptoms of schizophrenia (NSS) or Rett despite both being in Phase 3,” Hung said.

These additional Phase 3 programs could drive huge sales for ACAD, with Hung estimating that the figure could potentially reach $1 billion-plus. The analyst points out that even though Phase 3 data for trofinetide in Rett syndrome is slated for release in 2021 and the Phase 3 ADVANCE-2 study has kicked off, he is still cautious about the programs.

That being said, Hung thinks that “even with conservative 45-50% probabilities of success,” which are lower than the typical 65% he assumes for Phase 3 programs, he values them at about $6 per share on a risk-adjusted basis.

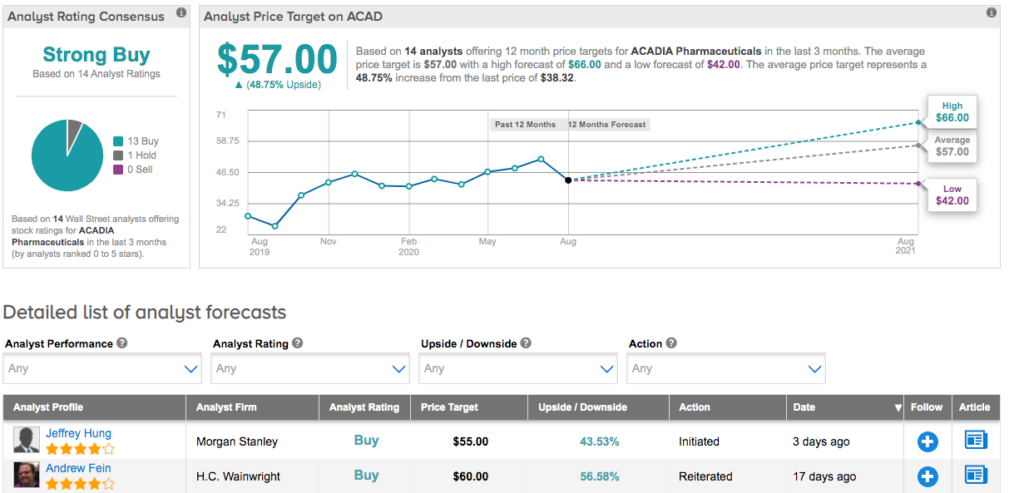

All of this convinced Hung to join the bulls. As a result, the analyst kicked off his ACAD coverage by putting an Overweight rating and $55 price target on the stock. Based on this target, shares could climb 44% higher in the next year. (To watch Hung’s track record, click here)

For the most part, other analysts agree. Out of 14 total reviews published in the last three months, 13 analysts rated the stock a Buy while only 1 said Hold. Therefore, ACAD is a Strong Buy. The $57 average price target is more aggressive than Hung’s and implies 49% upside potential. (See ACADIA Pharmaceuticals price targets and analyst ratings on TipRanks)

Pandion Therapeutics (PAND)

Developing innovative modular therapeutics based on its patented TALON (Therapeutic Autoimmune reguLatOry proteiN) drug design platform, Pandion Therapeutics wants to improve outcomes for patients with autoimmune and inflammatory diseases. Given the potential of its lead asset, PT101, Morgan Stanley thinks that big things could be in store for this biotech.

Representing the firm, analyst Vikram Purohit tells clients that PT101 is being evaluated in inflammatory bowel disease (IBD) ulcerative colitis (UC), which he argues “represents an area of significant unmet medical need.”

Looking more closely at the candidate, PT101 is an engineered form of the IL-2 protein termed an IL-2 mutein, which has been designed to overcome the dosing challenges posed by traditional low-dose IL-2 therapy. “We expect PT101 to be the key fundamental driver of PAND in the near-term with Phase 1 healthy volunteer data expected in 1H21 and UC patient data expected by 2022,” Purohit commented.

According to Purohit, part of what makes PAND stand out is its development approach, which focuses on designing three types of drug components (effectors, protein backbones, and tissue tethers) that can be combined to create therapies that exert either a systemic or a tissue-specific effect. PT101 falls into the first category, with earlier efforts from the TALON platform presenting “optionality through the potentially broadly applicable pathways being evaluated and the company’s efforts to develop tissue tethers that could provide Pandion’s drugs organ-selective impact.”

What else is behind Purohit’s bullish approach? He argues data for low-dose IL-2 therapy in UC shows the proof-of-mechanism for PT101. Additionally, based on preclinical data, the candidate has a broad and safe dosing profile.

As for its earlier-stage assets, Purohit believes they could be significant upside drivers if PAND can provide “strong proof-of-concept data for one tissue tether, as this would increase investor confidence in the company’s ability to design organ-selective therapies broadly, and a positive concrete update (such as the nomination of a candidate progressing into preclinical development) from the Astellas partnership, as Type 1 Diabetes represents an area of high unmet need and Pandion could earn significant milestone payments and royalties through its deal with Astellas.”

It should be noted that PT101 updates and competitor IL-2 data sets could have an effect on investor sentiment, in Purohit’s opinion. “We would expect investors to become more focused on the IL-2 space as more mature Phase 1/2 data becomes available from Pandion, Amgen, Roche, Lily/Nektar, and BMY throughout 2021, and we believe the set-up heading into these readouts is positive given the encouraging initial data in humans presented by Lily/Nektar and Amgen and given the nascent stage of interest in IL-2 therapies for autoimmune disease,” he explained.

Everything that PAND has going for it keeps Purohit with the bulls. To this end, he reiterated an Overweight rating and left the $25 price target unchanged. This target conveys his confidence in PAND’s ability to surge 38% in the next twelve months. (To watch Purohit’s track record, click here)

Other analysts don’t beg to differ. 4 Buy ratings and no Holds or Sells have been assigned in the last three months. So, PAND is a Strong Buy. The $26.50 average price target suggests 46% upside potential. (See Pandion Therapeutics stock analysis on TipRanks)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.